Gold Fuels Liftoff, Strategy Pulls Ahead of S&P 500

A relentless gold rally has powered the Asymmetric Edge strategy ahead of the benchmarks I track, including the S&P 500, with consistent gains across several timeframes.

Welcome! Before we get started, for anyone new or looking for a refresher, this newsletter focuses on making a top-tier investment strategy easy to understand by showing how I manage my own portfolio. Each month I share the four ETFs I hold and the percentage of my portfolio in each.

At a Glance

In this issue, I introduce a simpler newsletter format, share my thoughts on gold’s rise, review last month’s market moves, and look at how my portfolio strategy continues to outperform its benchmarks.

Market Movement Summary

- Gold launches to new highs

- The Asymmetric Edge strategy outperforms the S&P 500

- Volatility hits stocks for the first time in weeks

Portfolio Shifts

- Small allocation adjustments, same ETFs

- Monthly rebalance helped capture recent gains in gold and the Nasdaq

Theme of the Month

An investment strategy based on the idea that the US dollar will lose value over time because of government debt and money printing. Investors buy assets like gold, real estate, or foreign currencies to protect their wealth as the dollar’s purchasing power falls.

One Number That Matters

The wealthiest 10% of households now account for half of the country's consumer spending - Bloomberg

Market Moves

Portfolio & Benchmark Returns

The Asymmetric Edge strategy has delivered higher returns than the comparison benchmarks across the periods shown — three months, year-to-date, one year, and since inception in January 2024.

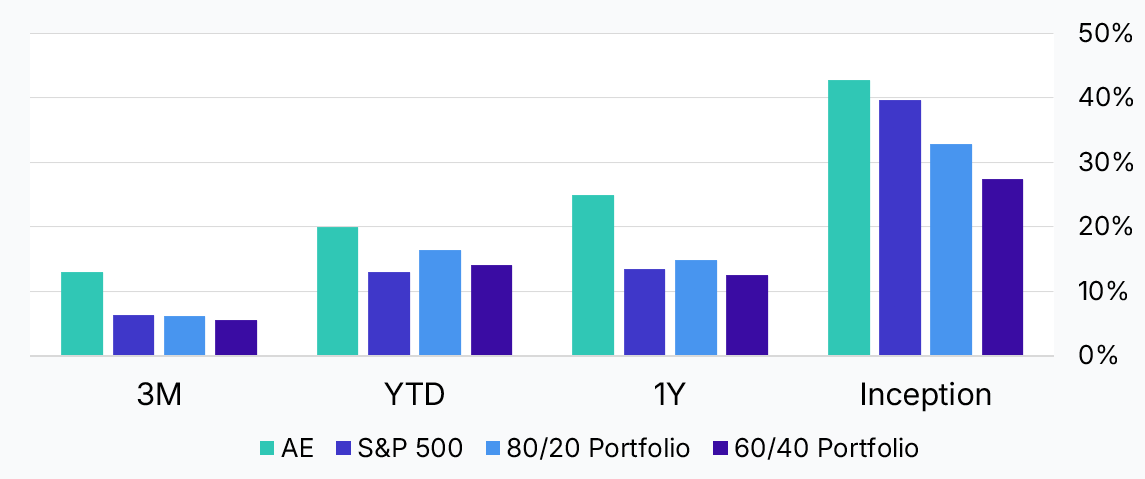

Another view of the same periods for comparison.

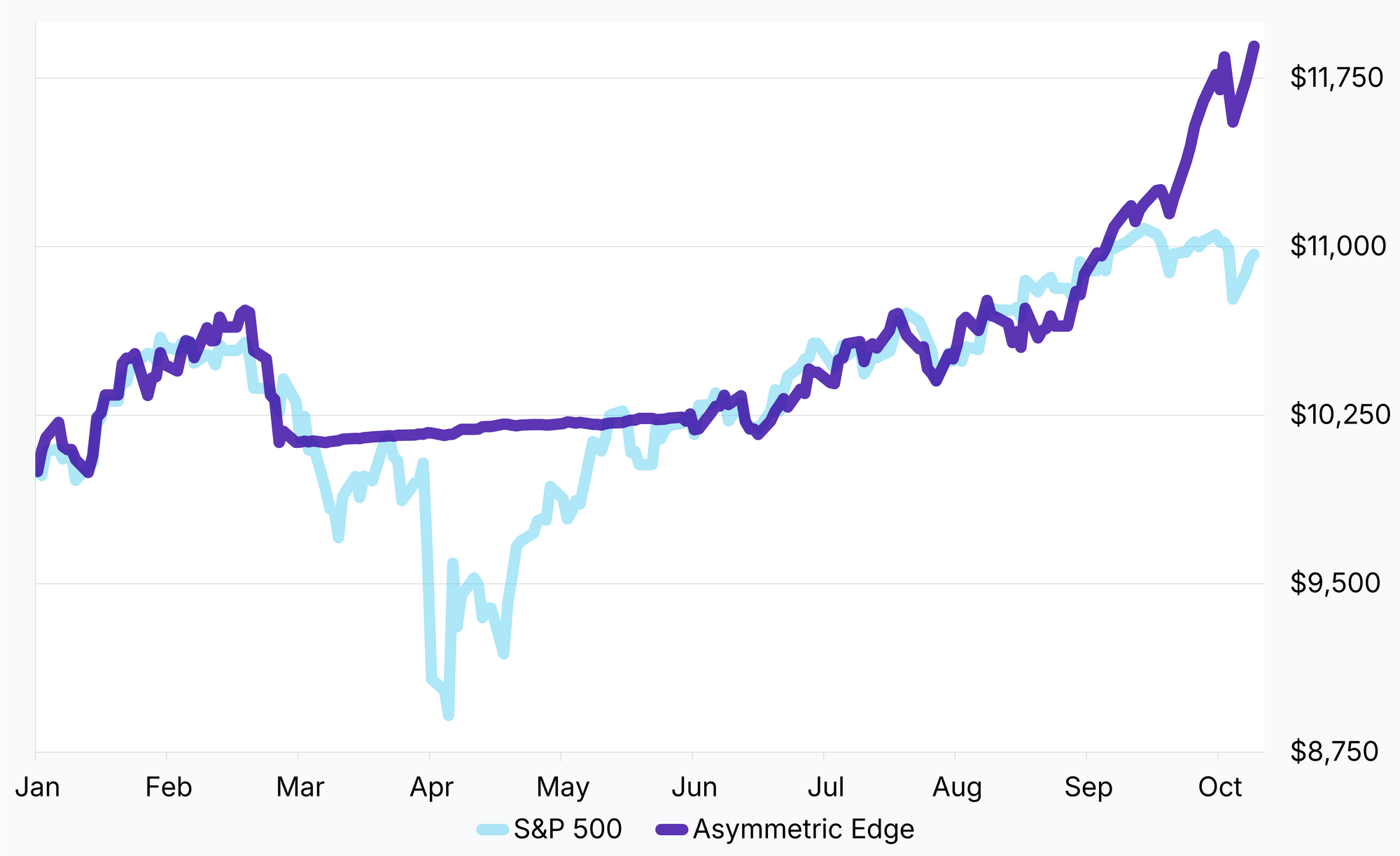

A Much Smoother Ride

For the periods shown, my strategy has had lower realized volatility than the S&P 500 and a smaller maximum drawdown. The chart above shows the value of including risk-off assets within a relative strength momentum rotation system. Its maximum drawdown has been less than half that of the S&P 500, with a peak to trough decline of 3.16% compared with the S&P’s 7.53%.

At the start of the year, the portfolio held positions in the Nasdaq-100, Russell 2000, gold, and bitcoin. As momentum faded, especially in the Russell 2000, short-term T-bills rose into the top four ETFs by relative strength. The strategy shifted about 97% into cash-equivalent T-bills for three months, sidestepping most of the market’s decline. In June, it rotated back into risk-on assets, tracked the rebound through August, and began outperforming again in September.

Beating the S&P 500 is not my goal. My focus is on matching or exceeding the returns of traditional stock and bond portfolios while doing so with shallower drawdowns. That said, I'll happily take these results.

Trailing 3 Month Returns

Allocations went out to paid subscribers last month, but since I didn't send out a newsletter, this issue looks back a bit further and uses a trailing three-month window for asset returns.

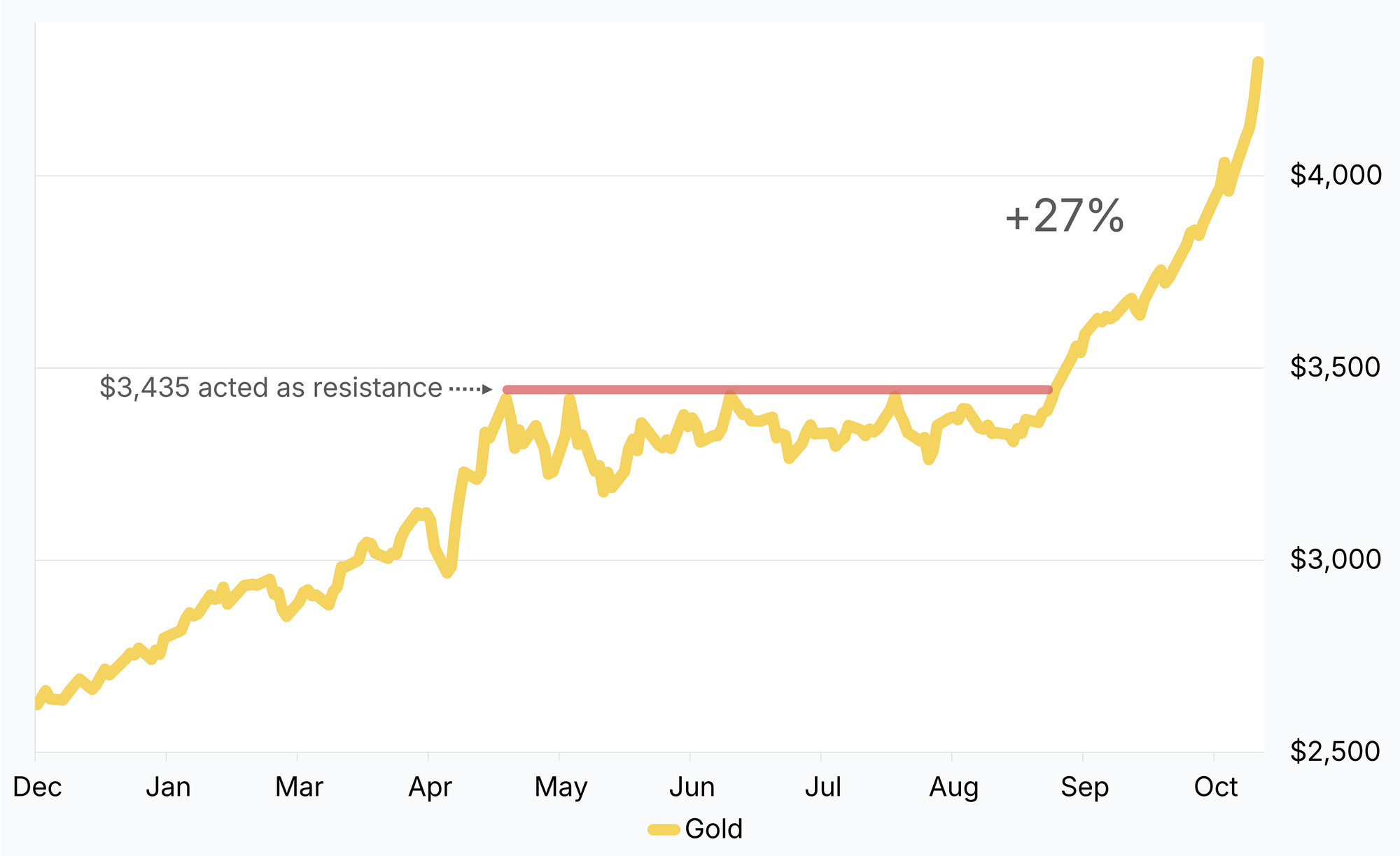

September marked a turning point for gold. After months of consolidation, it broke out and is up over 27% since then. With about 40% of the portfolio in gold recently, it has been the main driver of Asymmetric Edge’s outperformance.

U.S. markets saw volatility return on the 10th after a steady September climb. Pullbacks in uptrends are normal, and more downside wouldn’t surprise me before the next leg higher.

Bitcoin hit a new all-time high just over $126,000 before experiencing a significant decline. It looks weak for now, but if any asset can catch up quickly, it's crypto.

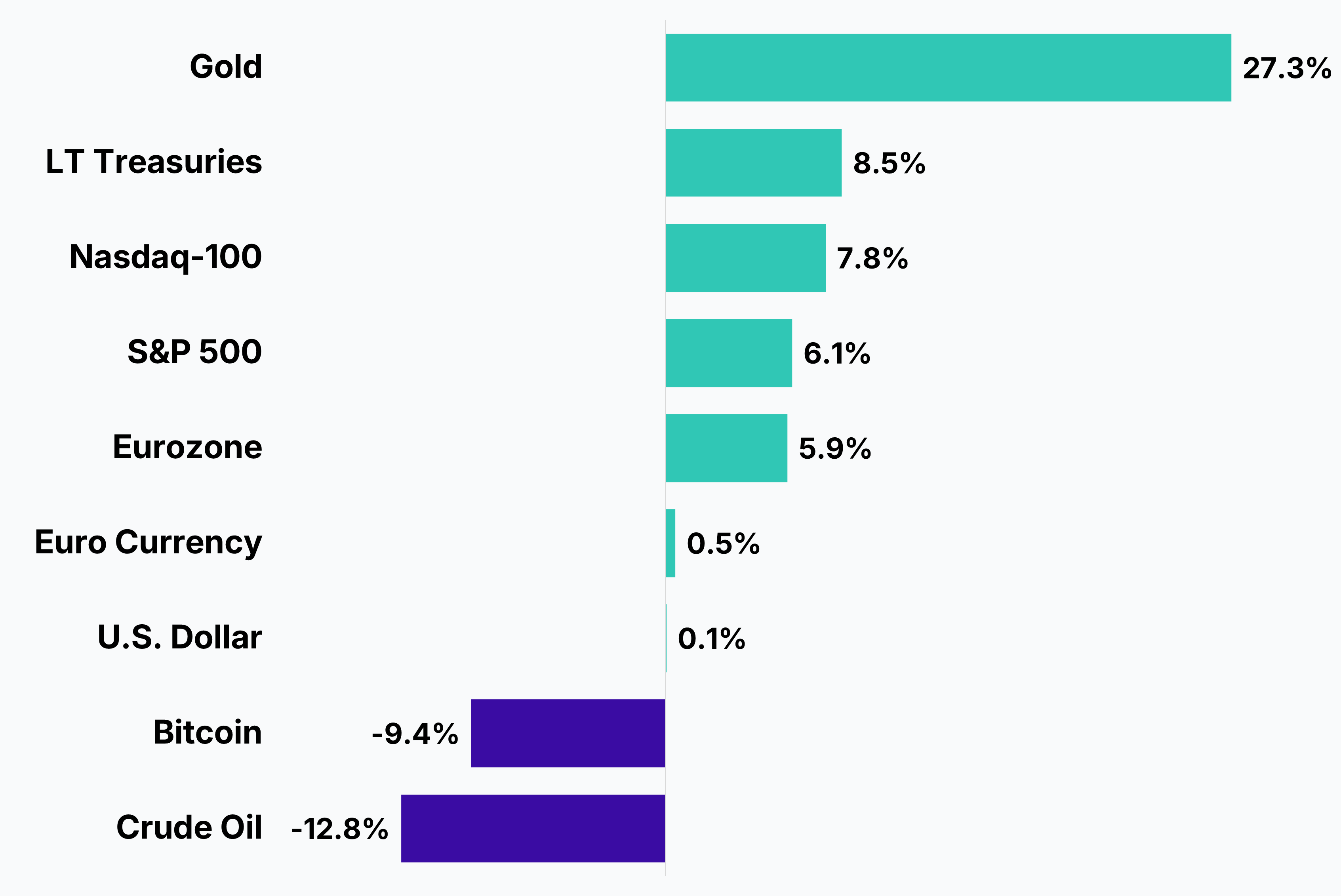

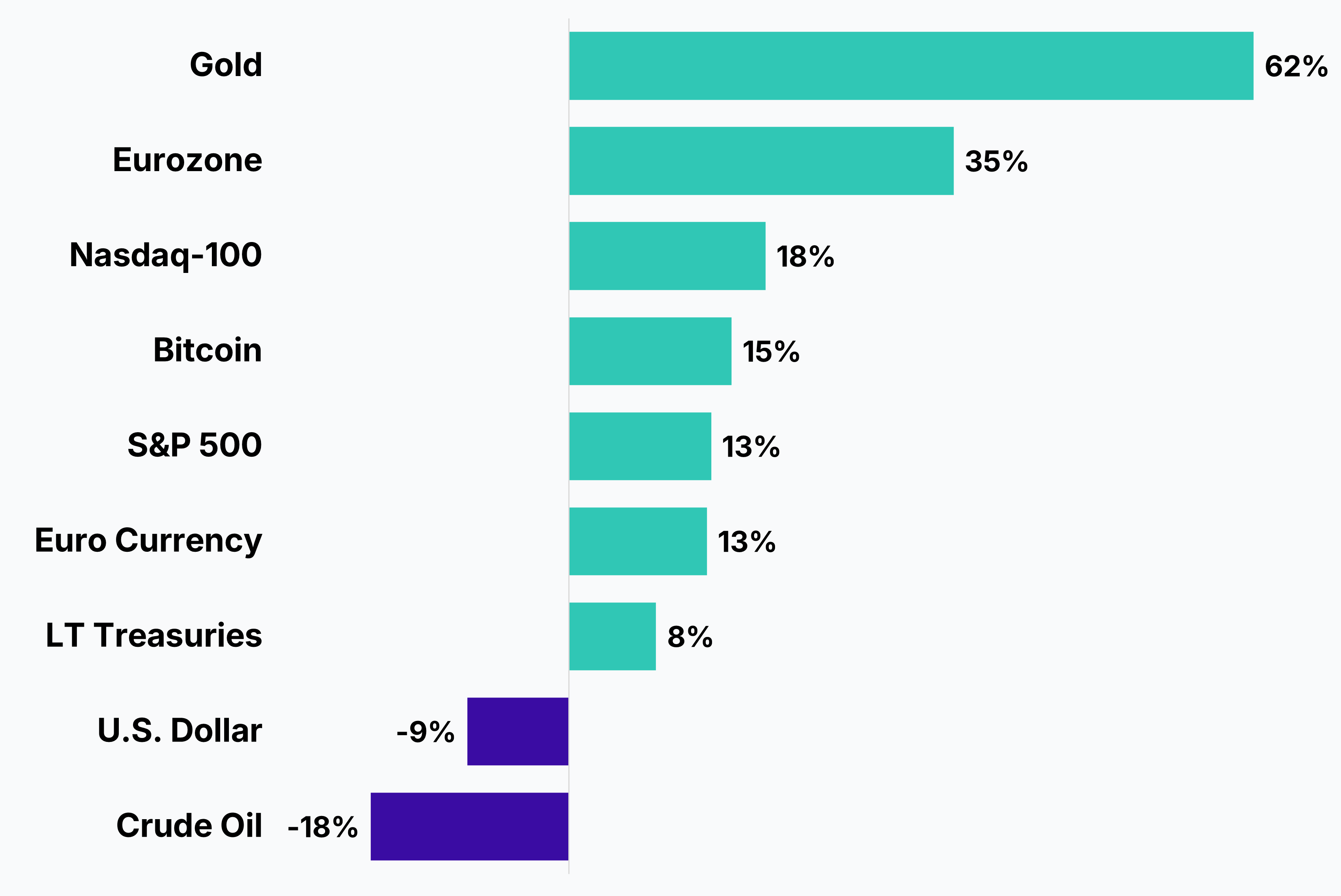

Year-to-Date Returns

Here you can see gold’s outperformance so far in 2025, up more than 62%. This chart demonstrates why I prioritize investing across a wide range of asset classes, not just stocks and bonds. Otherwise, I would have missed out on the current gold bull market.

Eurozone equities have been sluggish recently but still lead U.S. markets this year. I continue to watch the U.S. dollar closely, but the index has remained in roughly the same range between 96 and 100 since June. That’s fine with me, since dollar stability prevents the kind of broad market pressure that often comes with sharp USD rallies.

Oil prices continue to slide, making filling up at the gas station noticeably cheaper.

Portfolio Allocations for October

| Asset | Ticker | Weight | Purpose |

|---|---|---|---|

| 🟨 Gold | GLD | 39.2% | Inflation & crisis hedge |

| 💶 Europe | EZU | 25.9% | Diversification & USD hedge |

| 💻 Nasdaq | QQQ | 22.1% | Growth from US tech leaders |

| 🟠 Bitcoin | IBIT | 12.8% | Speculative growth |

Allocation changes were minimal this month, with slightly less going to gold and Eurozone stocks, and more in Nasdaq and bitcoin.

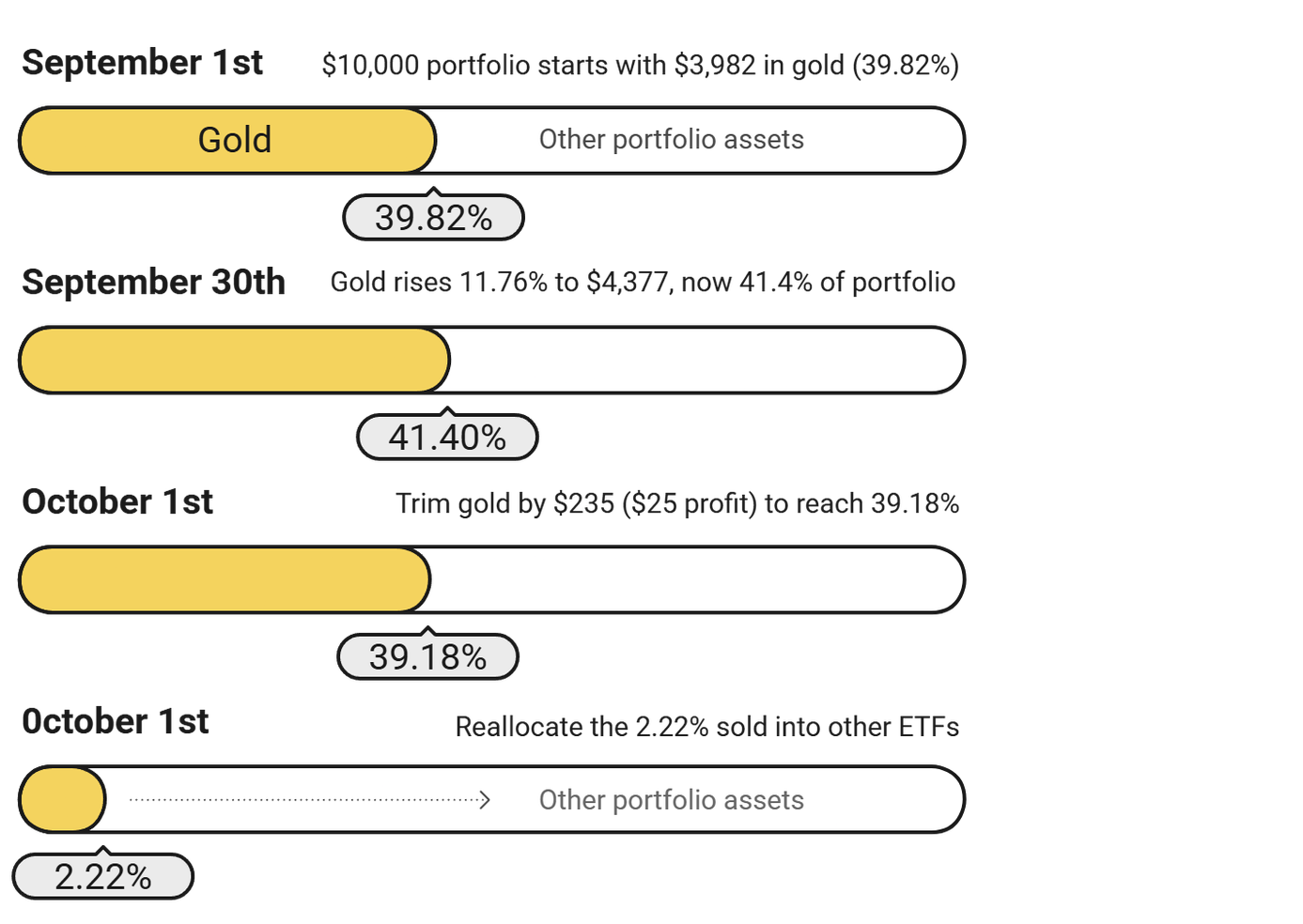

Monthly Rebalancing Locks in Gains: Gold as an Example

October’s rebalancing shows how the strategy steadily locks in gains on portfolio assets which have increased in value during the preceding month. A $10,000 portfolio starting September with $3,982 in gold (39.82%) would see gold rise 11.76% to $4,377 (41.4%). Trimming back to its 39.18% October target allocation means selling $235 worth of gold, realizing $25 in profit, and reallocating that money to other assets, methodically locking in gains on outperformers.

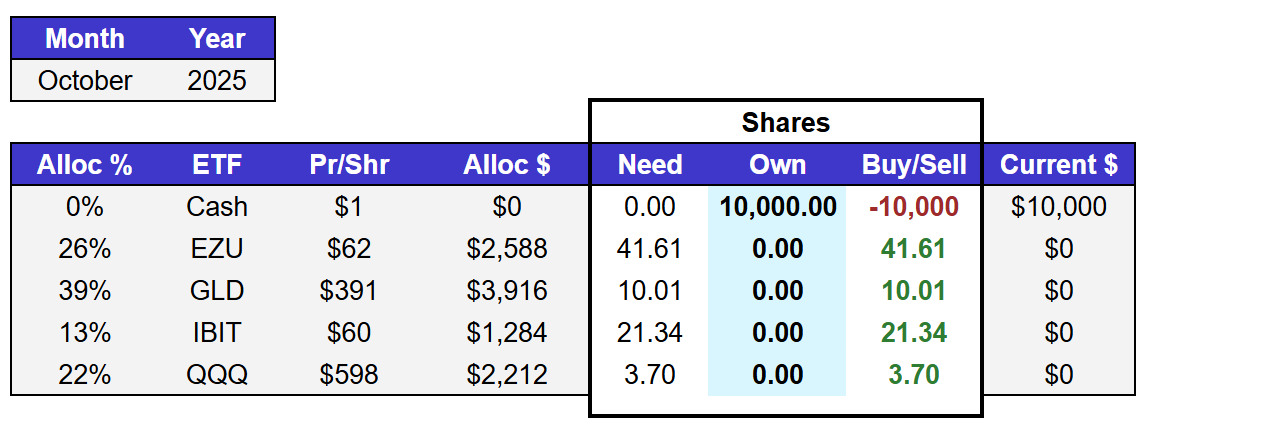

Purchasing Shares

Here you can see the spreadsheet calculator I use to rebalance my personal account. It pulls in near real-time ETF prices.

Educational tool that illustrates a rebalance calculation, not a directive to transact.

Calculator Terms of Use

This tool is for my personal use and shared for informational purposes only. While I strive to ensure accuracy, I make no representation or warranty as to its accuracy or completeness. Users should verify all calculations independently. Please consult your own advisor before using similar tools.

Inside the Strategy

I’m working on creating a static page in addition to my "about" page, that more fully explains how the Asymmetric Edge strategy works. I hope to have it live in the next month or two.

I’d love your input. What parts of the strategy still feel unclear?

A Note on Gold and Fear

When gold rises, it’s rarely for good reasons. Fear, currency weakness, and geopolitical stress often drive its gains. I’m positioned to benefit, but it’s bittersweet. Most of my exposure is through ETFs and futures contracts, though I also hold some physical gold. History shows why, during wars and crises, gold has often been the only way people preserved their wealth.

I see gold as another asymmetric bet. It makes up only a small share of my total assets, but in the kind of scenario where it’s truly needed, that small position could become incredibly valuable.

Fear of Loss and FOMO

It’s easy to watch assets like gold go parabolic and then immediately start worrying about when it will crash. I’ve felt that fear myself. More than once in recent weeks, after watching gold go up day after day, I was tempted to cash out entirely or sell part of my position. If I had done that, FOMO would have kicked in as gold continued to climb. Once you are out, deciding when to get back in is nearly impossible.

This is when having a thoroughly tested strategy is so important. I’ve spent years refining mine, and while I continue to monitor and improve it, I’ve found it is usually best to trust my analysis, sit on my hands, and follow the process I created instead of reacting to the market. Doing so has paid off in the past and especially in recent months.

Wrap Up

I’m continuing to refine the format of these newsletters as I optimize over time. They were getting a bit lengthy and time-consuming to write, so I’m aiming for shorter, more focused updates going forward.

Let me know what you think of the new format and design. My goal remains the same: to share my portfolio strategy in a clear, approachable way, demystifying investing and opening access to an exceptional, research-based system.

This newsletter is for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. The information contained herein has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Opinions expressed are subject to change without notice. This material is not an offer to sell or a solicitation of an offer to buy any security.

The author may hold positions in securities mentioned in this newsletter. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Investment involves risk, including possible loss of principal. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.