Doing Nothing Was the Hard Part

The strategy is up 23.0% year-to-date, more than double the 80/20 benchmark's 9.5%. Inside: the quiet handoff of market leadership to small caps and emerging markets, and why three months of doing nothing was the hardest part.

At a Glance

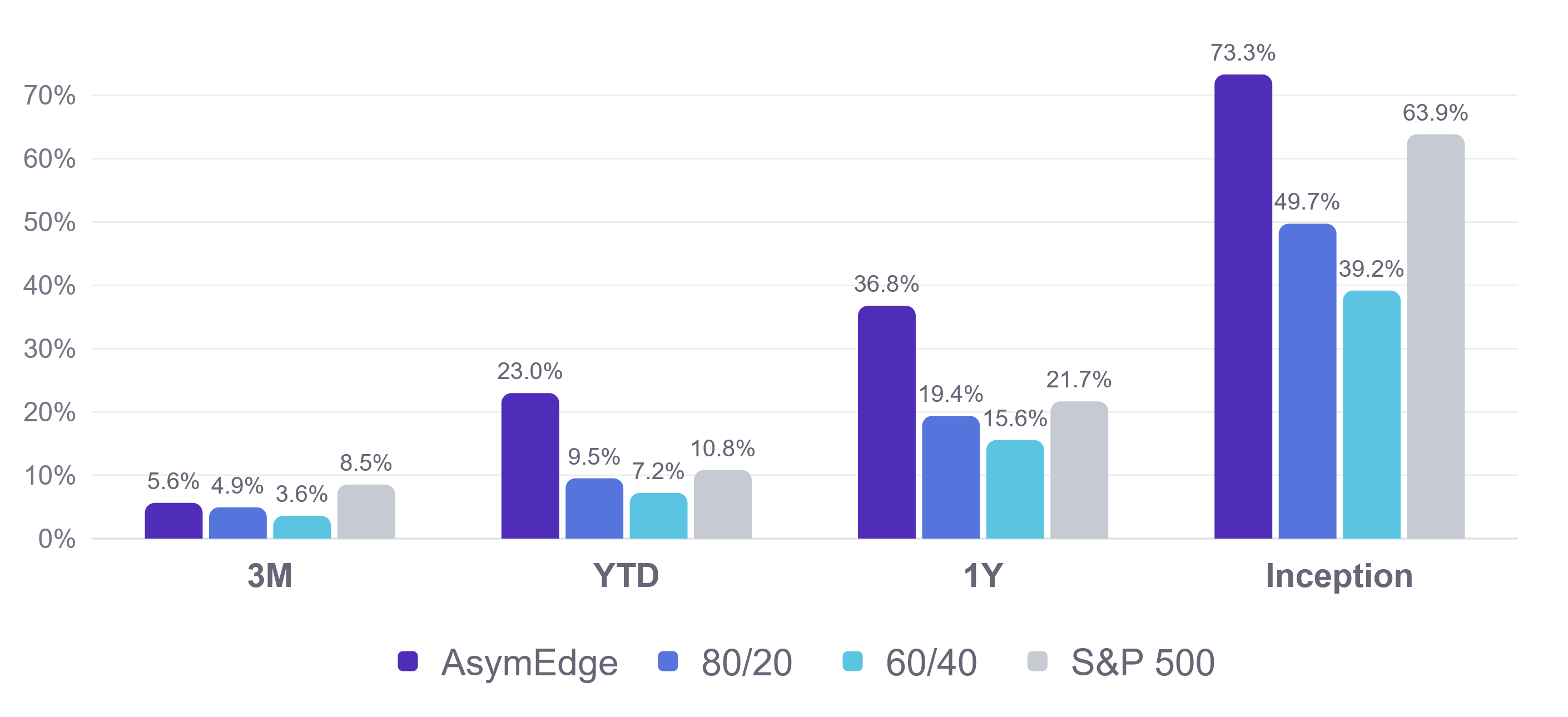

The Asymmetric Edge strategy is up 23.0% year-to-date, more than double the 9.5% return of its 80/20 benchmark, after a first half in which market leadership quietly changed hands.

This issue walks through a milestone first half for small caps and emerging markets, the July rebalance that kept the same four ETFs for a third straight month, and a deep dive on why doing nothing is often the hardest part of a rules-based system. There is also a short macro check on inflation, jobs, and the Fed.

📌 This newsletter documents how I invest my own money with a simple, rules-based strategy. The aim is to match a traditional balanced portfolio with shallower drawdowns, and I share what I hold and why so you can watch it play out.

Market Movement Summary

- 📈 U.S. stocks set records, with the Dow closing above 53,000 for the first time and the S&P 500 finishing the first half up 9.6%.

- 🔷 The Russell 2000 posted its best first half since 1991, up nearly 22% through June, as AI infrastructure spending spread to small-cap suppliers.

- 🌏 Emerging markets ex-China gained 32.80% year-to-date, and EM funds took in $38 billion of new money in the first half, more than all of 2025.

- 🏭 Commodities led every major asset class, with crude oil up 38.17% year-to-date amid the ongoing Middle East supply disruption.

- 🔥 Inflation re-accelerated through spring, with May headline CPI hitting 4.2%, before June's print cooled to 3.5% as energy prices fell during the ceasefire.

Portfolio Shifts

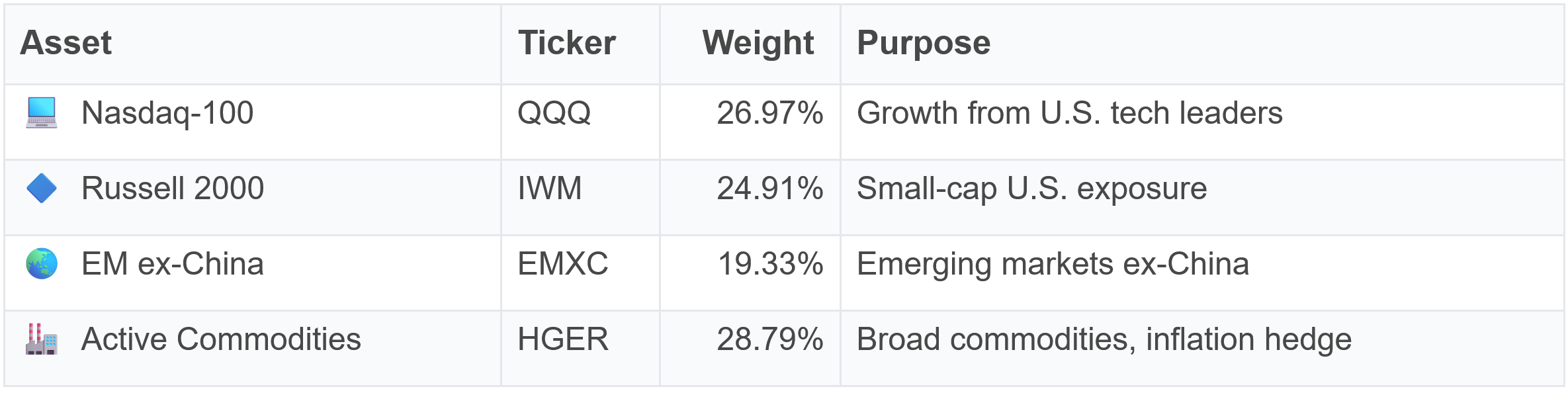

- No ETF entered or exited at the July rebalance. The same four positions carry into a third straight month.

- The rebalance topped up active commodities after a weak June and trimmed emerging markets ex-China, whose higher volatility caps its weight.

- Since the rebalance, commodities have run ahead while the equity positions have pulled back, so the weights have already drifted. More below.

Theme of the Month

The handoff that happens when the assets pulling the market higher stop being the ones that led before. This year the S&P 500 has done fine, but small caps, emerging markets ex-China, and commodities have done far better. A portfolio built to follow relative strength was already positioned in the new leaders before the handoff made headlines.

One Number That Matters

The Russell 2000's first-half gain, its best start to a year since 1991. Small caps spent years overshadowed by the mega caps. This year they have led the U.S. market for two straight quarters, and this portfolio has held them the whole way. (Source: CNBC)

Market Moves

Portfolio and Benchmark Returns

The gap is not subtle this year. The strategy's 23.0% year-to-date compares with 9.5% for the 80/20 portfolio, 7.2% for the 60/40, and 10.8% for the S&P 500. The pattern holds over longer windows too, 36.8% over the trailing year versus 19.4% for the 80/20, and 73.3% since inception against the 80/20's 49.7% and the S&P 500's 63.9%.

Risk-adjusted, the year looks even better. The Sortino ratio (return earned per unit of downside risk, where higher is better) sits at 7.27 for the strategy year-to-date against 1.86 for the 80/20, and the deepest month-end drawdown so far this year was 3.60%, shallower than the 80/20's 5.24% and the S&P 500's 5.76%. In fairness, the strategy's worst single day (down 4.97% on January 30) was deeper than anything the benchmarks saw, the price of running a concentrated four-position portfolio.

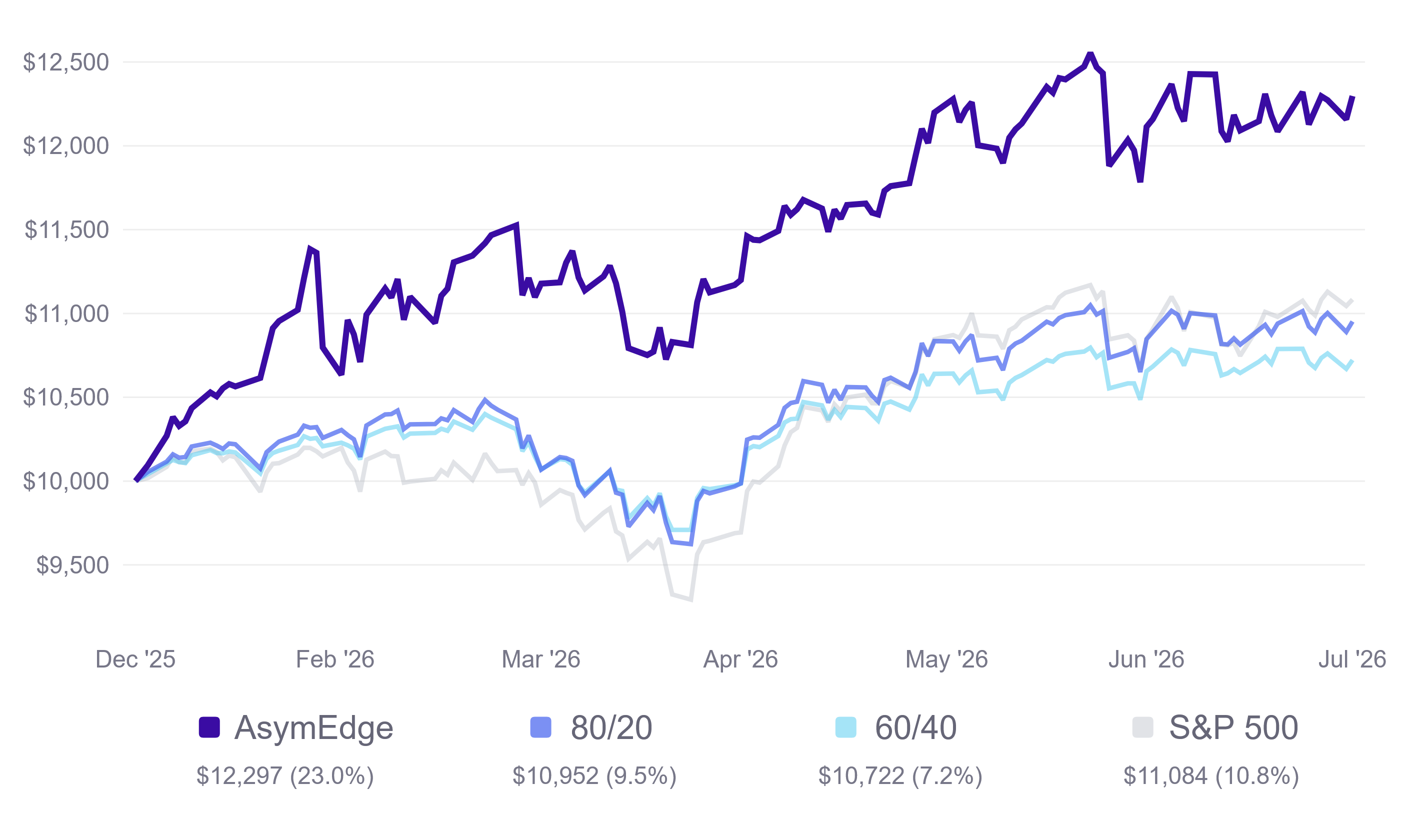

Charting the Growth of $10,000

In dollar terms, a hypothetical $10,000 invested at the start of the year would now be worth about $12,297 in the strategy, versus $10,952 in an 80/20 portfolio and $11,084 in the S&P 500. Stretch the window to a full year and the same $10,000 grows to about $13,680 in the strategy against $11,940 for the 80/20 and $12,170 for the S&P 500.

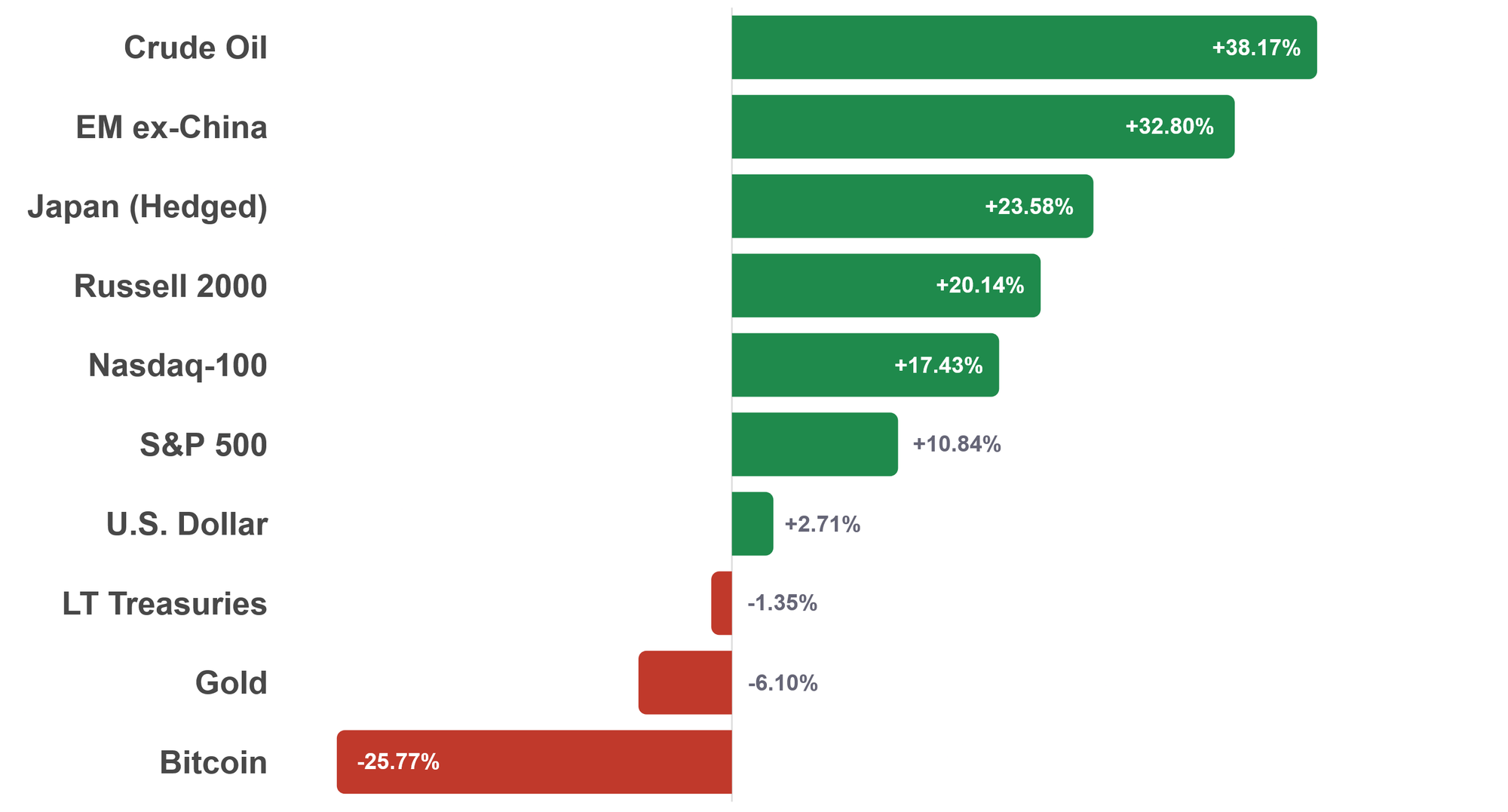

Year-to-Date Asset Class Returns

Crude oil leads everything at +38.17%, with emerging markets ex-China (+32.80%) and currency-hedged Japan (+23.58%) close behind. Small caps (+20.14%) and the Nasdaq-100 (+17.43%) run ahead of the S&P 500's +10.84%. At the bottom sit long-term Treasuries (-1.35%), gold (-6.10%), and bitcoin (-25.77%). The rankings are why gold and bitcoin are not in the current lineup.

The dollar has also climbed nearly 3% from a four-year low, a reversal that usually works against commodities and international assets. That both kept leading anyway says something about the strength of their trends.

Small Caps' Historic First Half

The Russell 2000 just posted its best first half in 35 years. This is not a meme-stock rerun. The AI buildout is spreading beyond the mega caps, with chip-related names accounting for 16 of the index's 50 best performers this year (CNBC). Small caps have been roughly a quarter of this portfolio all year, so this was one rally you did not have to chase.

Commodities Keep Carrying Their Weight

The all-weather commodity fund (HGER) is the portfolio's largest position and its best performer this month, up 7.63% since the July rebalance while all three equity positions pulled back. Oil supply has stayed disrupted since the ceasefire collapsed in early July. I will spare you the war headlines. The commodity position keeps doing its job, performing when inflation is the market's main worry.

Inflation, Jobs, and the Fed

The macro picture explains a lot of the rotation. Inflation ran hot through spring, with May headline CPI at 4.2%, the highest since 2023. The June print, released July 14, eased to 3.5% as energy costs fell during the ceasefire, and core came in at 2.6%. The relief could prove temporary. Oil has climbed again since the ceasefire collapsed in early July.

The job market is cooling too. June payrolls rose just 57,000, down from May's 129,000, with unemployment at 4.2%. The Fed held its rate at 3.50% to 3.75%, meets again July 28 and 29, and futures markets still lean toward a September hike. The 10-year yield near 4.6% helps explain why bonds and gold have struggled while real assets and stocks with strong earnings have led.

Portfolio Allocations

Same four ETFs, third month in a row. The July rebalance was a tune-up, topping up active commodities after a weak June and trimming emerging markets ex-China. The sizing comes down to risk parity, weighting each position to contribute a similar amount of risk to the portfolio. Commodities, the least volatile of the four, get the most dollars, while top-ranked EM ex-China's higher volatility caps its weight.

Deep Dive: Boredom Is a Position

The strategy has now held the same four ETFs for three straight months. That stretch included an oil shock, a second wave of inflation, and a string of record highs in the indices. Through all of it, the portfolio barely moved.

I want to be honest about how that feels, because patience might be the most underappreciated skill in investing.

The itch to do something

Markets are built to feel like they demand a response. Every headline arrives with an implied question, are you going to act on this? When your portfolio answers no for ninety straight days, a specific discomfort sets in. It does not feel like patience. It feels like negligence, like being the only person at the party standing still.

That discomfort has a name, and it is not prudence. It is boredom. Boredom is one of the most expensive emotions in investing, because the natural cure for it is trading.

What the itch costs

The classic study here is Barber and Odean's "Trading Is Hazardous to Your Wealth," which followed tens of thousands of retail brokerage accounts through the 1990s. The most active traders earned roughly 11% a year net of costs while the market returned close to 18% (Barber and Odean, 2000). The households that traded the most were not less informed than the ones who sat still. They were less able to sit still.

That finding has held up in the decades since, and the mechanism is not mysterious. Every unnecessary trade is a chance to be wrong twice, once on the exit and once on the re-entry, with costs charged both ways. Activity feels like control. Mostly it is leakage.

A counselor's reframe

In my counseling work there is a skill called urge surfing. An urge behaves like a wave. It builds, crests, and passes on its own if you can watch it without acting on it. The skill is not suppressing the urge. It is noticing it, naming it, and letting it finish its arc while your hands stay still.

Watching a portfolio do nothing for three months is urge surfing with money. The urge to tinker shows up on schedule, usually right after an urgent headline or a big red day. I have learned to treat it as information about me, not information about the market. The market did not send me a signal. My nervous system did.

What three quiet months actually did

Here is the reframe that makes the boredom bearable. The portfolio was quietly productive for three months. The system ran its full ranking process three times, compared every asset in its universe, and concluded three times that the same four ETFs were still the strongest. A decision was made every month. It just remained the same decision each month.

And while the lineup sat still, market leadership quietly moved toward exactly what the portfolio already held. Small caps had their best first half since 1991. Emerging markets ex-China climbed to the top of the asset class table. Commodities led everything. None of it required a single move from me, because the relative-strength rankings had put the portfolio there before the story was obvious.

That is the trade-off a rules-based investor accepts. You give up the entertainment of doing something, and in exchange you get a shot at being early without needing to be clairvoyant. Some months the discipline of doing nothing is the entire job.

The desire for constant action irrespective of underlying conditions is responsible for many losses in Wall Street, even among the professionals. - Jesse Livermore

A century old, and it could have been written about this exact stretch. The past three months have been pretty boring, but this is often how it goes with investing.

Wrap Up

If you have spent this stretch watching war headlines next to record highs and feeling like you should be doing something, that restlessness is normal, and it is exactly why I follow a systematized, rules-based approach that takes the emotion out of my investment decisions. I will run my portfolio model at the end of this month as I always do. If the leaders keep leading, the portfolio will keep holding them, and if they fade, it will move without asking how I feel about it. Either outcome is fine with me. The job is to stay in the game and follow the process.

Disclaimer & Disclosure

This newsletter is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer to sell or buy any securities. The content is published as a journal of the author's personal investment activities and is intended for a general audience.

No Investment Advice: The author is not a financial advisor. You should not treat any opinion expressed herein as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of opinion.

Risk Warning: Investment involves risk, including the possible loss of principal. Past performance is not indicative of future results. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

Data & Accuracy: Information contained herein has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. All expressions of opinion are subject to change without notice in reaction to shifting market conditions.

Positions: The author currently holds positions in the securities mentioned in this newsletter. The author may buy or sell these securities at any time without notice.

Copyright: This content is provided solely for the personal use of the subscriber. Any unauthorized copying, forwarding, or distribution of this material is prohibited without prior written consent.